Introduction

In the words of the Billionaire Carlos Slim, Courage taught me no matter how bad a crisis gets … any sound investment will eventually pay off. These words perfectly highlight the need to learn Financial Literacy for Beginners. We need to master financial management so that we avoid spending too much money or get into debt. For example, if someone loses track of their money and does not save, they may be unable to cover important expenses or emergencies, resulting in a financial disaster.

Let’s start to learn Financial Literacy! Financial literacy is the capacity to understand and use financial abilities, such as budgeting, investing, and so forth. It also requires knowledge of some financial theories and concepts, like interest rates, debt management, the time value of money and much more.

People can avoid making bad financial decisions by becoming aware of their finances.. It can help people become self-sufficient and financially secure. Learn how to make a budget, track spending, pay off debt, and plan for retirement. Educating yourself on these topics also includes knowing how money works, being careful of scams and developing financial objectives.Knowing the fundamentals of investment, interest rates, and other financial concepts is part of understanding how money works. Additionally, one needs to learn how to handle financial challenges that arise in life and become aware of scams. Financial objectives can help you chart a path toward your financial objectives.

One life skill that allows people to live comfortably is financial literacy. It can assist someone in overcoming obstacles in life as well as pursuing their goals. It leads to the possibility of a secure life to take care of your family during medical emergencies or any other mishaps. In this blog, we will look at a few key steps to learn the basics of financial literacy.

- How to create a budget for beginners

In the words of Warren Buffett, “Do not save what is left after spending, but spend what is left after saving.” Knowing every aspect of your finances and how you want to spend them is the objective of a budget. A budget is a personal way of accounting for all of your money, including your salary, any additional income you may receive from investments, etc. As much as 70% of Americans believe that budgeting helps them maintain their financial stability. If you’re not currently on track to complete your goals, you can learn to make some adjustments with the help of a budget. Here are some budgeting tips for beginners :

- Track your income and expenses: Know exactly how much you earn and where your money goes each month.

- Use the 50/30/20 rule: Allocate 50% for needs, 30% for wants, and 20% for savings and debt repayment.

- Set realistic financial goals: Create short-term and long-term goals to guide your budgeting efforts.

- Prioritize savings: Treat saving like a monthly bill—pay yourself first before spending.

As mentioned, one method to evaluate your existing finances is to apply the common 50/30/20 budgeting model. This strategy aims to give 50% of your post-tax income to necessities (rent, food, and auto payments) and 30% to necessities (phone bill and streaming services) or “nice to haves” (expensive dinners, for example). The remaining twenty percent is saved for things like emergency funds, retirement funds, and a down payment on a new car or house.

Read Also: Financial Planning vs Retirement Planning Made Simple

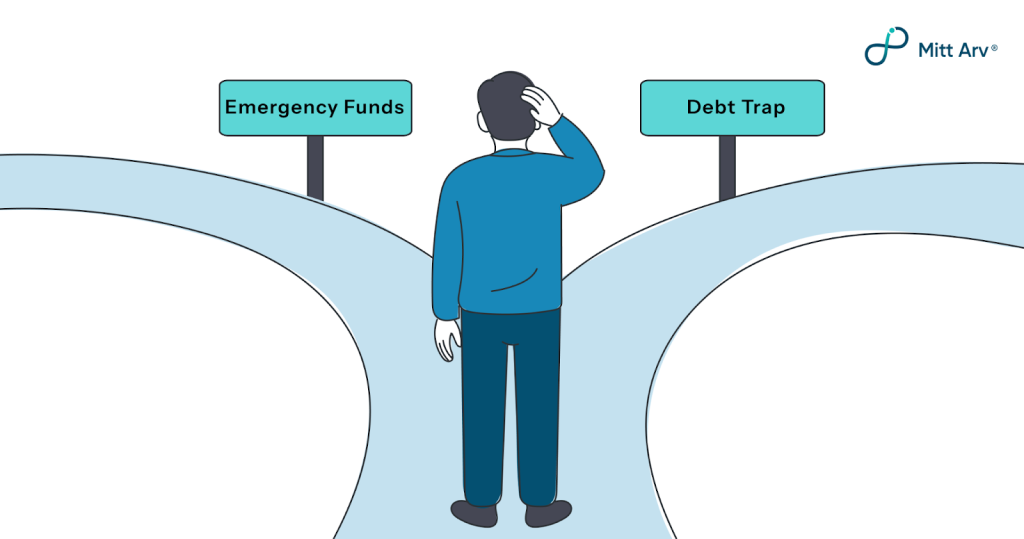

- Best tips to save for emergencies

Dave Ramsay once said “You must gain control over your money, or the lack of it will forever control you.” The phrase perfectly emphasises the importance of emergency fund because even little crises can result in stress and debt. Being in charge of your money indicates that you are prepared for the unexpected. Here are some extra tips for your emergency fund :

- Start small and stay consistent: Even small amounts saved regularly can build up over time.

- Open a separate savings account: Keep emergency funds separate to avoid accidental spending.

- Automate your savings: Set up automatic transfers to your emergency fund every month.

- Cut unnecessary expenses: Identify and reduce non-essential spending to boost savings.

Establishing a target for the amount of savings is the first step in creating an emergency fund. It is good to have at least three to six months’ worth of living expenses saved in an emergency fund is a good idea.

Six months’ savings for costs provide more than enough security in most cases. Savings for emergencies become more important if you have children or an unpredictable income. An emergency fund might reduce financial stress during difficult times and prevent you from relying on high-interest debt. Remember to separate this fund from the rest of your investments. Start with small savings and make regular contributions; even small amounts add up over time and bring comfort. Keep in mind that each tiny action you do today advances your financial goals.

Read Also: Preserving Legacies: Inheriting Assets and Taxation as an NRI

- Track and Change

Regularly checking your financial condition is important for staying on track with your goals. This includes analysing your bank statements and reviewing your budget. Life is continuously changing, and your financial plan should change with it. Major life events, such as starting a new career, getting married, or having children, may require changes to your budget and priorities. A bigger salary, for example, may allow you to increase your savings or pay off your debt more quickly. Staying aware of personal finance and obtaining expert guidance as needed will help you make sound, confident financial decisions over time. Here are some ways to track and change your finances :

- Regular financial check-ins: Review your bank statements and budget regularly to stay aligned with your financial goals.

- Adapt to life changes: Adjust your budget after major events like starting a new job, getting married, or having children.

- Utilise salary increases wisely: Use any raises to boost savings or pay off debt instead of increasing spending.

- Be mindful of daily expenses: Cook at home instead of frequently ordering food online to save money.

- Trim unnecessary subscriptions: Reduce or cancel unused streaming services and memberships to cut costs.

Keeping up with your budget can have a significant impact on your finances. For instance, cooking at home instead of ordering food online can eventually save a lot of money. If you reduce your streaming package or cancel any unused subscriptions, you can save extra money. Received a raise in pay? Increase your savings or pay off debts instead of increasing your spending. Reduce your spending on entertainment and clothing if your rent has gone up. Your budget should adapt to the changes in your life. Frequent check-ins help you identify leakage, establish new objectives and maintain financial management rather than allowing it to dominate you.

- Steps to Avoid Debt Traps

Taking debts and rash purchases can lead to poverty. It is critical to educate oneself on budgeting, saving, and spending wisely. Financial education enables you to make sound decisions and avoid debt traps that jeopardise your long-term security and progress. Here are the steps to avoid debt and build wealth :

- Borrow only when necessary: Take loans only for important needs like education, home, or emergencies.

- Understand the terms: Always read and understand loan agreements, interest rates, and repayment schedules.

- Keep EMIs manageable: Make sure your EMIs don’t exceed 20–30% of your monthly income.

- Pay on time: Always pay your EMIs and credit card bills before the due date to avoid penalties.

Sometimes, taking out a small loan appears to be an easy answer. But beware: this can soon lead to too much debt. Never take out a loan to settle present debts. You should only take out a loan for something necessary, such as education or medical bills. Sometimes you truly want something, and that’s fine. You should still compare costs online and, in certain cases, simply wait till the item goes on sale. When shopping at the supermarket, it can be helpful to make a shopping list, take note of any deals in advance, and focus on what you need. It’s also a good idea to sign up for bonus programs and check digital vouchers regularly in the apps.

- Retirement Planning

Although we know there will be no guaranteed income when we retire, most of us postpone our retirement savings plans until later in our careers. It is necessary, yet it is hated. For this reason, retirement planning is the most essential financial choice. According to data by the RBI, 23% of Indians have formal retirement planning, and 37% are unwilling to save for it. Let’s look at the best tips for retirement planning :

- Start early: The sooner you begin saving for retirement, the more time your money has to grow through compounding.

- Set clear retirement goals: Estimate how much money you’ll need for the lifestyle you want after retirement.

- Contribute regularly: Make consistent contributions to retirement accounts like PPF, EPF, NPS, or other pension plans.

- Maximise employer benefits: Take full advantage of employer-sponsored retirement plans and matching contributions.

- Diversify investments: Balance your portfolio with a mix of stocks, bonds, and other assets based on your age and risk tolerance.

Experts caution that pursuing comfort and enjoyment in one’s youth at the expense of saving for the future can result in financial ruin when one is unable to work or make money. To avoid this, the best course of action is to plan ahead of time and begin investing for retirement.

Don’t forget to keep inflation in mind. You may combat inflation by choosing a retirement plan that can withstand rising prices. Make sure there is an “increasing sum assured” option in the retirement plan you select. This type of protection plan will offer life insurance with yearly increments to mitigate the effects of inflation. You can also get advice from a financial expert to help you make an investment that generates returns higher than inflation rates.

Read Also: Retirement Planning: Top 10 Common Mistakes to Avoid.

Conclusion

Not only is financial literacy a practical ability, but it is also essential in today’s fast-paced, uncertain world. By learning how to manage money, save for emergencies, and avoid excessive debt, you take control of your financial well-being. Whether you’re just starting or wanting to improve your financial habits, it’s never too late to begin your journey. Start with the basics: develop a budget, maintain an emergency fund, and make conscientious spending choices. Stay informed, change your financial plans as your life changes, and always keep your long-term goals in mind. Understanding how to improve financial literacy enables you to make wise choices that safeguard your future. It shall benefit the next generation for their betterment.

Saving money for yourself is only one part of financial planning; another is supporting your future family. You create a solid foundation when you learn how to save and make wise financial decisions. This could end up being your own legacy. You can provide a better life for your kids if you manage your finances effectively. In addition to providing for their necessities and education, you can also teach them sound money management techniques. They will pick up on your habits and become more life-ready. Additionally, you can steer clear of large debts to spare your family from future hardships. Your family can concentrate on their aspirations and ambitions rather than worrying about bills.

FAQs.

How much should I save in an emergency fund?

Ideally, save 3 to 6 months’ worth of your essential expenses for unexpected events like job loss or medical emergencies.

How to improve Financial Literacy?

Improve financial literacy by budgeting, tracking expenses, adjusting plans, avoiding debt, and regularly learning about savings, investments, and retirement planning.

How can I avoid falling into a debt trap?

Borrow only when necessary, repay loans on time, use credit cards wisely, and always plan your finances carefully.

What are some easy ways to start saving money?

Set automatic savings transfers, cut unnecessary expenses, track your spending, and wisely use cash-back or discount offers.